It’s challenging to measure as it requires predictions on what avoidance schemes, etc, are available under the new rates and how those apply or don’t to those in the new higher rates. That is, you have to figure out what the actual effective tax rate will be for those being hit by the new rates. That’s really, really hard.

Agreed. I think that’s part of the idea behind the wealth tax; to tax the people who otherwise wouldn’t be. I’ve heard much less about that, however, so I kind of assume it’s a non-starter.

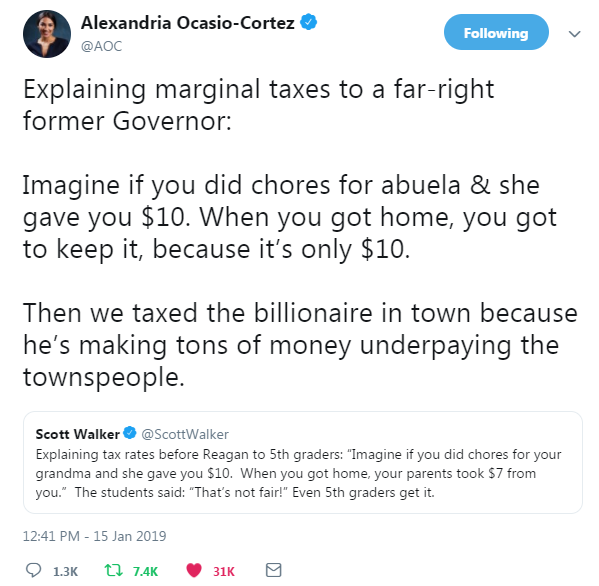

I haven’t read a concrete proposal yet. My assumption (possibly wrong) would that a top rate rise would be accompanied by marginal rate rises across the income spectrum, ie. above $5m is taxed at 50% and so on. Hopefully it would include a rise in the capital gains tax as well, given that’s where rich chiselers make the majority of their money.

Well social security has totally separate accounting. The general fund is never used to pay social security appropriations. But yeah, funneled into income and food security programs, infrastructure (=jobs), health care, research, etc, it could do lots of good.

I can pretty much guaranty you that taxing earnings in excess of $10 million per year at 70% would generate at least the $5 billion needed to fund Trump’s wall. ;-)

So I have a weird question for health insurance industry-watchers

My job and I combine to spend around $600 biweekly toward insurance (health/vision/dental - not including life in this). It’s a flat amount for full time employees and totals up to about $31,200/year. My plan covers both myself and my kid (he’s under 26, thankfully). Some employees have many more for the same amount (it’s a three-tiered system of either employee, employee + kids, or employee + kids + spouse).

In 2017, the US health insurance industry reported about $880 billion in revenue. If the expenses toward my health insurance is fairly similar to others, that revenue would be met by a little under 30 million policies. That number seems … low?