Near as I can tell, it’s another negotiating tactic, like the pie-in-the-sky Paul Ryan budget, which required moonbeams and unicorns to work. They’re drafting a bill which will allow “more leeway” in specifying what gets cut, while keeping the amount cut in the Sequester. No details on what “more leeway” means, so it’s not anything resembling full discretion, and thus not meaningfully different than the present plan, just a way to pretend that the specific cuts were the Democrat’s idea.

That said, I’m having trouble seeing how changing the targets would help even if they were allowing full discretion. Firstly, it’s not discretionary spending that’s the problem.

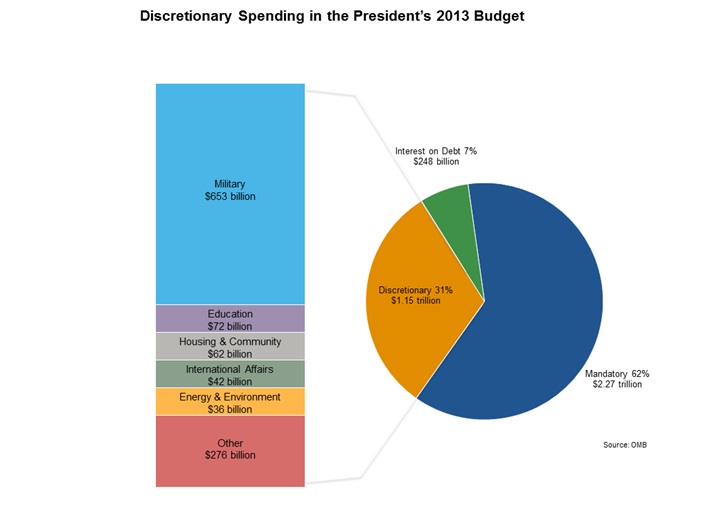

The first rule of optimization is “measure.” If a process is taking up only 31% of your clock cycles, you can’t save more than 31%. You always examine the biggest chunk first.

Second, within discretionary, by far the biggest chunk is military. If you cut discretionary spending by $85 billion, the Pentagon has to be most of it. Most of the economic effects being discussed are about the results of the non military cuts on the economy, like cutting back the FAA and fewer air traffic controllers.

We could cut that much, if we’d just stop fighting wars overseas.

It’s just an attempt to rig the blame game. One of the problems the Republicans have, in retrospect, is that sequestration (sequester is a verb goddammit) hits all programs at a fairly granular level. The Republicans would love to put the President in a position where he has to make the choices, because then they can say “President Obama cut your favorite program instead of this shitty program.”

The problem is the assumption that we NEED to reduce the deficit right now, which both sides share.* WE DON’T. It’s just “r-word” to believe it. Some days I just feel like taking my head in my hands. Why does everyone keep behaving as if we lived in the pre-1971 “gold window” currency regime?

*I realize that the moral panic about it by the Republicans is at least partly just a way of keeping the Administration from proposing spending programs they’re not comfortable with ideologically.

I agree that we don’t need to reduce the deficit right now, and that this is a particularly bad time to be discussing it. On the other hand, I’m not a fan of debt on the personal level, and thus I get the emotional appeal of “we need to reign in our overspending.”

Of course, the national debt is not exactly like personal debt. It is debt, and it is a matter of spending more than we’re taxing, but when articles talk about our per-capita share of the debt being $52k per person, that conveniently ignores the fact that taxation is not allocated that way. Long term, the effects of increasing the debt will be higher taxes on the rich. Because, as Sutton’s Law states, “that’s where the money is.”

I’m not a fan of debt on the personal level either (I drive a 15 year-old car), but our national debt is a qualitatively different thing. These people who keep predicting the rise of the “bond vigilantes” and hyperinflation are completely oblivious to the fact that we don’t live in a precious metal-standard currency regime any more (and thank God for that). How do they explain the case of Japan, which has a debt to GDP ratio which dwarfs our own, and yet, hey, no hyperinflation!

My total debt right now is exactly equal to my mortgage. And if I had a regular job, I’d pay that off, despite the tax advantages. So I completely agree on personal debt, too.

It’s the plain-talking common-sense millionaires and billionaires in congress who piss me off, because they know very well that the nature of debt is different when you have leverage on your creditors, even at their personal levels, much less on the national level where money itself is defined by act of law. But still they get up on their hind legs in front of the cameras and try to talk about the deficit as if it was a heavy credit card balance – not that they themselves ever owe money except when it’s in their advantage to do so.

I’m not so sure why the Republicans like this. If I were Obama, I’d be saying, “Hmmm… Texas, you clearly don’t need those bases, Mexico’s not going to invade us anyway, I’ll send it over to Massachusetts. Arizona, same deal, your money goes to NY. Now, which Republican districts are next?”

What’s the worst that happens – Texas won’t vote Democrat in the next election?

With 5% of the discretionary budget set to be cut, there’s almost no way for the President to avoid pissing off someone. Right now he gets to hide behind the wording of the law; you can’t blame him if the shit you like gets cut. If he’s got discretion, you can blame him.

I’m really not sure that it’d work in the GOP’s favor even if the President had to come up with the specific cuts (the lessons of the 90s suggest it wouldn’t), but who knows. Right now though, the way sequestration is implemented lets the President almost totally wash his hands of responsibility.

Let’s digress here for a moment: Gus points out above that the national debt is debt. This is true insofar as the federal government owes its creditors back a certain number of US dollars in principal, plus whatever interest it agreed to pay them, also in US dollars. The US government, while it remains sovereign, cannot be forced to repay its debts in anything but US dollars. But what gives those dollars their value? Only the willingness of producers of goods and services to take those units in exchange for said goods and services, and the willingness of US governments at all levels to accept them as THE way of extinguishing tax obligations. That’s all that gives a fiat currency its value. You could view US dollars as shares that let you participate in the US economy, and to the extent that foreigners accept USD, the world economy. They’re just a way of “keeping score” and facilitating trade/exchange, and that’s it.

So, while it’s important that the value of US dollars not be diminished by too many of them being issued such that they outstrip production, their value is also determined to a great degree by how robust the US economy is in terms of production, innovation and employment. Which is why it’s unbelievably short-sighted to freak out about the very remote prospects of bond-vigilante-ism and significant inflation when we could achieve full employment and improve our infrastructure in a few years by just spending as necessary at the federal level.

People say “but we’re burdening future generations of Americans with debt!!1!” Really? Are they gonna have to put food and cars and toys and clothes and computers into time machines in 2063 to pay off today’s bondholders? Of course not. Today’s bondholders are mostly very wealthy people, institutions and governments who find themselves with scads of dollars, and their choices are to invest them (which involves risk), sit on them at 0% return, or park them in Treasuries to get as close to a risk-free return as there is to be had. When they redeem their Treasuries, they’ll get their principal and their interest as agreed (unless the Teatards keep the debt ceiling from being raised) and even more people/institutions/governments will line up to buy more Treasuries. We’ll NEVER collectively have to pay it all off at once, EVER.

Really? Never all at once, I can stipulate to that, but I’ve seen the argument that it’s okay to do absolutely nothing about the debt because you never need to repay it all. So you kick the can, you raise the ceiling, you do absolutely nothing about it. The American model is unsustainable. Increase your damn taxes, for a change.

The other problem is that your flippant attitude to debt is backed by the all-too-American belief that you can get away with it because you can bully foreign lenders into submission. I’d like to see what would happen if a weaker country attempted the same. Actually, maybe you’ve heard of the incident where a hedge fund, Elliott Management, had a vessel of the Argentinian Navy detained in Ghana over distressed debt. Well, these fuckers, with a track record for doing stuff like that since the mid-nineties, tried every trick in the book:

Elliott Capital and other holdout bondholders have been tracking Argentine assets, financial and physical, closely, sources said. Back in 2007, a group of bondholders discovered that the Tango 01, Argentina’s presidential airplane, would be in the U.S. for scheduled maintenance and pilot training. They moved to get a court to keep the plane grounded after it landed and to seize fuel money the pilots were expected to bring in cash. The government of the late Nestor Kirchner was warned of the move, though, and cancelled the trip. It then countersued in the U.S. getting California judge William Alsup to declare the presidential Boeing 757/200 was immune from seizure.

It’s not only vehicles they were after. In 2009, Argentina was preparing a stand at the world’s largest book trade convention, the Frankfurt Book Fair. Rumors that assets could be seized forced Argentine to register its stand under a private individual rather than the state, and a showcase of works of art requested by German curators was withheld given concerns they would be seized. A year later, a Tango 01 trip to Germany was cancelled just as Buenos Aires was warned it would be seized.

Holdout bondholders have also gone after the assets of prominent Argentine politicians, including Nestor Kirchner, his wife and current president Cristina Kirchner, and 136 members of her administration, including most of the cabinet. In 2010, Singer’s Elliott got Judge Griesa, who consistently rules against Argentina, to ask Bank of America to disclose all information related to their personal accounts. Elliott has even gone after Argentina’s foreign exchange reserves, coming close to seizing $105 million held at the Federal Reserve Bank of New York.

While most of their attempts to grab Argentine assets have failed in court, Elliott and other distressed debt investors have recorded some victories. Having bought the debt originally for pennies on the dollar, their strategy is to pursue aggressive means to recover a greater amount.

Argentina appealed to the Tribunal for the Law of the Sea Convention (yes, there is actually such a body) in Hamburg, which in mid-December ordered Ghana to release the ship. Before the Ghanaian courts could even consider whether the Tribunal’s ruling should be given effect in that country – a question as to which there was considerable doubt, given that Ghana has enacted no substantive law providing that orders of relief from this body supervene the decisions of the Ghanaian courts – Argentina grabbed its ship and skipped town.

Yes, you prick, there is such a thing as international treaties, and Ghana (but naturally not the Amurricans) actually ratified that convention (and had a judge on the tribunal until 2005).

Argentina couldn’t do anything against Elliott because those politically connected fuckers are protected by American law. And if you tried to do anything against these fuckers, you would have to face the brunt of the American diplomatic and military force. But that, you see, could never happen to the United States, even if they defaulted. Just imagine seizing the USS Constitution during a goodwill tour – no country would dare. Worse is that – of course – all the comments at the links I posted, Forbes and Business Insider, are massively on Singer’s side, to the point of refusing to compensate Ghana for the costs associated with detaining the vessel. And that’s how you get away with things.

So, as one of America’s foremost intellectuals might have said: When you come to a sequester in the road, take it.

Re: "bullying foreign lenders: Look, no one forces Chinese electronics manufacturers, for instance, to take US dollars in payment for their offerings. They could insist on payment in Yen, or Euros, or gold bullion or whatever, but they don’t. They then end up with dollars piled up in accounts somewhere. They can do whatever they please with those dollars–no one is forcing them to buy US debt instruments, but sometimes they do because in their judgment it’s their best alternative. As long as the inmates* aren’t running the asylum, everyone will get back their dollars with interest when the bonds mature, so what’s the problem? I’m not seeing one.

And please explain to me how continuing to raise the federal debt ceiling as necessary is “unsustainable” (thanks for the link to the Atlantic article BTW)? Insofar as spending enough at the federal level to goose aggregate demand when necessary maintains and improves reasonable economic growth, I’d say it’s the very definition of sustainable. Tax revenues rise when there’s prosperity. Not that the federal government actually needs our dollars except as a way of creating demand for the currency itself (and regulating its supply among the users of said currency).

I think that’s actually been made illegal after Nixon tried that. That said , if things have to be cut, making it where Tea Party states go bankrupt would be something I’d do ruthlessly.

Highly amusing to read laughable comments like this even as I am watching Italian bonds blow up as a result of the election there yesterday. Government spending rarely covers cost of capital. Without the Germans funding massive buying of Italian/Spanish/Portuguese bonds through the ECB, all of these countries would already be in default.

Hello, how can you ignore the fact that Italy is not a sovereign fiat currency issuer, and thus has debt denominated in something it can’t control. It makes ALL the difference in the world. How many times does this blindingly obvious fact have to be repeated, hmm? Highly amusing, indeed.

If their debt was not denominated in euros and backed by Germany they would never have been able to borrow the amounts they have already borrowed, nor would they be able to roll over their existing debt. You are basically saying they needed to borrow less and spend less than what they already have, and implement austerity much sooner and harder that what they already have. I agree.

No, not saying that at all. I’m saying that if they’d never given up their monetary sovereignty (I assume back in the late 90’s or whenever) they probably wouldn’t have gotten into the situation where they needed to borrow so much in the first place, which only became necessary because a currency union without a full fiscal union (a central taxing and spending authority) is a mind-bogglingly stupid move. It’s as if we had the US dollar but no IRS and no Congressional spending to balance out the inevitable imbalances of payments that would arise among the states. How soon would Mississippi, Oklahoma et al be in thrall to California, Washington state, New York, Massachussets etc.?

Also, a government which fully controls its own currency has MUCH greater fiscal flexibility to deal with business cycle fluctuations than one that does not. Austerity is not the only tool available to it.

Needed to borrow? They didn’t need to borrow. They wanted to borrow so they could live beyond their means. Just like the Greeks did. Thanks to the euro they were able to spend away while borrowing on a scale and at a cost they could only have dreamed of prior to the euro. Of course the money was all pissed away, because pissing away money is pretty much what governments do. Then, quite suddenly, confidence disappeared and the free ride was over, with jack and shit to show for it. Without The euro, and Germany and the ECB they would all be in default. Default being a bullet to the heads of their own economies since the biggest holders of any nations sovereign debt are as a rule the countries own banks/pensions/citizens.

And we come back around to the “spendthrift Greeks and Italians (and Spaniards and Irish)” and “government spending = waste” memes. No one held a gun to people’s and institutions’ heads and forced them to buy Italian and Greek “sovereign” debt (quotes around “sovereign” because, you guessed it, it’s not). Perhaps these governments didn’t “need” to borrow in the first place, but now, with 20%+ plus unemployment rates, and people committing suicide in desperation? Yeah, they need to. Which if they had never stopped using the drachma and lira, wouldn’t be necessary, because they’d have everything in their toolbox that a sovereign fiat currency issuer has, including deficit spending and rolling over debt in perpetuity.

Anyway, those countries are well and truly fcked–we’re in agreement as far as that goes. I don’t see how austerity will lead to prosperity–it just leads to higher unemployment/lower tax revenues/less GDP–a vicious cycle. Either there’s a full Euro-zone fiscal union (which will never happen) or those countries default and the the Euro pretty much collapses. And then Germany is fcked, because suddenly its exports fall off a cliff.

My point is that OUR country*, which hasn’t taken the boneheaded/moronic/benighted step of giving up its monetary sovereignty, has tools at its disposal that the Euro-zone countries don’t, despite all the squawking of the Austrian school types.